OK, so Bill Gates said that these banks are dinosaurs, and they’re going to be supplanted. So what do you think? Are they going to be supplanted by FinTech companies?

Mr Gates said that people don’t need banks to do banking, and that seems to be where the shift is going. We can’t think of anybody who enjoys lining up at a brick and mortar bank just to deposit or withdraw some cash. And even for the employees that work there, that’s not a pleasant experience. So there is the friction, and one approach that entrepreneurs take is trying to minimise such friction.

If we look at the wave of efficiencies that we’ve seen throughout history, as technology evolves, there is eventually pressure put on existing cost structures that things in theory should become more efficient. Therefore, as new technology comes into play, many banks are absorbing, or trying to absorb some of those technologies to reduce cost. Part of that comes from laying off people. Another part of that is trying to find technological solutions to allow them to lay off more people. That is what led to some of the scale and profitability that we referred to in the previous section.

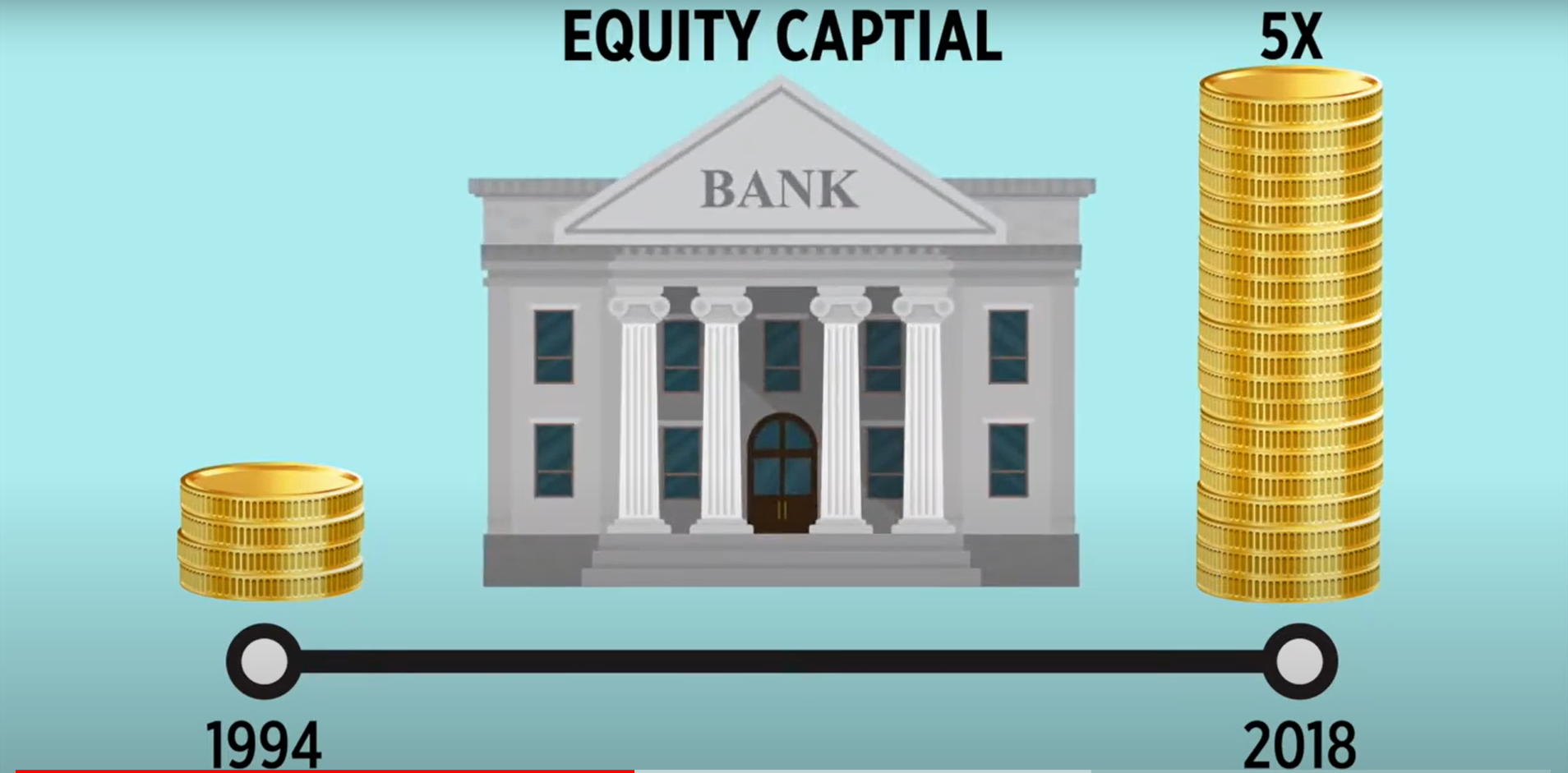

Research shows that the growth of the financial industry from 1994 to 2018 was indeed helped by the fact that there were significantly fewer actual bank entities, meaning, brick and mortar bank branches, and consequently, fewer employees that work in them.

If we think about technological evolution, there’ll be a lot of innovations that we can’t see as day to day consumers. But the point that we’ll all be able to see or we are already seeing is that there’ll probably be less and less physical presence. So going back to all the great experiences you had lining up at a traditional bank, that experience will be, hopefully less and less.

In fact, FinTech is introduced to push people away from that experience. Many banks now will actually charge you if you go to the bank branch for basic services. Whereas online banking allows you to transfer unlimited amounts for free. So over the past decade, banks have actually affirmatively been pushing people away from a business model perspective.

David Bishop first had an experience with a bank called ING Direct. It’s signatured with an orange card and the fact that there are no physical locations of the bank anywhere in the world. At the time, this was quite revolutionary. They were able to keep a very low cost banking, therefore giving you better interest rates. He was already banking through this kind of external system before he moved out of the US over a decade ago.

But what’s interesting about that is, ING Direct was tied to a traditional financial company. ING Group traces its roots to two major insurance companies in the Netherlands and the banking services of the Dutch government.

We’d like to think of FinTech as this disruptive force decentralising and democratising financial institutions, pulling away the traditional sources of power. But the reality seems that they are mostly utilised by traditional banks. Online banking was certainly not started by non-banks. And now traditional banking institutions such as JP Morgan have also entered the cryptocurrency space. So is FinTech a kind of a false vision of the future? Are we instead just seeing a retrenching of existing power bases, especially within the financial industry?

Well, we don’t think those paths are necessarily mutually exclusive. Banks in their current form, have existing customer bases and they need technology they can scale. A lot of the investments that many large international commercial and investment banks are making are into enhancing technology. And that could be realised either by in-house development or through acquisitions.

As an entrepreneur, you may have a vision of producing something to make the world a better place. But ultimately, if someone comes knocking and writes a big cheque to acquire this technology, it can be a very attractive proposition for an entrepreneur. Therefore, a lot of the innovative technologies will find themselves into established players.

But at the same time, there’s going to be a whole host of non-traditional financial players or institutions, who also get into and stay in the game. One example of that is PayPal. A lot of people look at PayPal as the first big domino in trying to get into this payment space, which has been traditionally dominated by more mature players who are not so savvy with technology.

Examples like that are more common in Asia in recent years. Ant Group, formerly known as Ant Financial and Alipay, Webank owned by Tencent, and KaKao Bank which originated from KaKao Talk are all aggressive players entering the financial world. Through accessible technologies and attractive fees and interest rates, their online user acquisition growth was rapid compared to traditional banks.